Liyan Yang, Haoxiang Zhu

Based on: Review of Financial Studies, 2020, 33(4), 1484-1533 DOI: https://doi.org/10.1093/rfs/hhz070

Imagine that Renaissance Technology, one of the most successful hedge funds, just bought a million shares of a stock. If that information tells you that the stock is more likely to do well in the future, you are not alone. Nor would you be surprised if the stock price has already trended up. While no one has a crystal ball to see the actual identities of buyers and sellers of financial assets in real time, a key function of financial markets is to figure out the information content behind buy and sell orders. Large institutional orders are particularly informative about asset fundamentals and future price movements. That’s why order flows of institutional investors are highly coveted information on Wall Street. While some investors try to uncover fundamental information about stocks, some others are “back-runners”: strategic traders who try to discover the trading direction of fundamental investors, anticipate their subsequent orders, and exploit such information. In response, institutional investors mitigate detection by randomizing the way they split orders. The presence of back-runners leads to delayed price discovery and significantly increases the value of order flows, including retail order flows that are uninformative about future price movements.

The anticipation of order flows has always been controversial. For example, Larry Harris, a former SEC chief economist, wrote in his book Trading and Exchanges, “(o)rder anticipators are parasitic traders. They profit only when they can prey on other traders.” In its Concept Release on Equity Market Structure in 2010, the SEC asked: “Do commenters believe that order anticipation significantly detracts from market quality and harms institutional investors?” The heat on order anticipation reached a new high when Michael Lewis, in his 2014 best seller Flash Boys, claimed that the U.S. stock market is rigged because high-frequency traders (HFTs) can use advanced technology to prey on institutional order flows. The word “front-running” is frequently used to describe order-anticipation strategies of HFTs, but a more accurate description is probably “back-running”: HFTs must first learn from public information about order flows before exploiting it. Consistent with the back-running interpretation, recent evidence reveals that HFTs start by providing liquidity to large institutional orders, but if the order takes several hours to fill, they trade in the other direction.

While certain HFT algorithms can detect large institutional orders directly, back-runners can also learn about institutional order flows by paying for retail order flow. In the United States, virtually all retail orders that can be immediately executed at prevailing market prices are routed to wholesalers such as Citadel Securities and Virtu Financial. In return, retail brokers receive payments from wholesalers. All off-exchange trades in the U.S. stock markets, including dark pools and retail orders, are reported together under the same category. Usually, one can’t tell which trades are retail and which are institutional. But, because Total Order Flow = Retail Order Flow + Institutional Order Flow, wholesalers that purchase retail order flow can tell the two components apart and gain an information advantage. The current SEC Chairman, Gary Gensler, commented in his written testimony on May 6, 2021: “the wholesalers get valuable information from this [retail] order flow that other market participants get with a delay, if at all.” Recent evidence reveals that the public reporting of off-exchange trades leads to a sharp burst in trading and quoting activity, suggesting that market participants learn from those reports.[1] Viewed this way, payment for order flow can also lead to back-running of institutional orders. The back-running aspect of payment for order flow can be highly profitable and deserves more attention from practitioners and regulators.

What are the consequences of back-running for institutional investors and the market overall? The short answer is that the presence of back-runners harms institutional investors, generates extra noise in institutional investors’ order flows, and leads to delayed price discovery in the stock market.

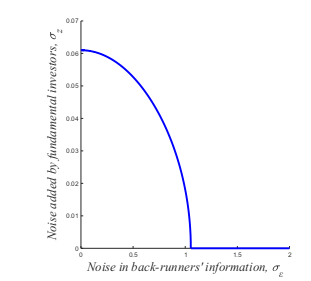

To explore these ideas further, suppose a fundamental investor wishes to buy a stock as long as its price is below a price target, say $12/share. In the morning, she uses a trading algorithm that chops a large order into small pieces and sends them off to various exchanges and off-exchange marketplaces. By the early afternoon, the stock price has gone up significantly, more than what she expects based on her total purchase. Upset, the fundamental investor calls the programmer of the algorithm and discovers, to her horror, that the algorithm sent out 5,000 small orders of 200 shares each at a regular interval of two seconds in the morning. Clearly, back-runners have detected the trail of breadcrumbs left by the algorithm and made a reasonable guess that a large buyer is lurking in the shadows. The algorithm is promptly fixed so that the timing and order sizes are randomized. From that day on, her trades leave no more breadcrumbs, just a scent in the air that only a very few lucky back-runners can sniff out and follow. Sometimes the back-runners dart off in the wrong direction. The fundamental investor misses the days when back-runners were not gazing and pacing near her gate, but the randomization machine serves as a useful defense strategy. She turns on the randomization machine when the back-runners get too close to her secret trades, as shown in the chart below.

The presence of back-runners reduces the profit of fundamental investors and, by leading to the strategic randomization of order execution, delays price discovery. That is, a larger fraction of fundamental investors’ private information is revealed later, rather than earlier. Because back-runners become partially informed about the fundamental value of the asset, price discovery eventually improves despite the delay. Applied to a trading day, the emergence of back-runners implies that price discovery shifts toward the end of the trading day, and the end-of-day price becomes more predictive of subsequent prices. Applied across days, it implies that price discovery prior to earnings announcements shifts closer to the announcement day, and earnings announcements become more informative about firms’ fundamentals.

What is the value of retail order flows in the U.S. stock market? We apply the back-running model to quantitatively estimate it. Bloomberg reported in 2017 that the payments received by leading retail brokers in the United States are in the order of tens to hundreds of millions of dollars per year. In the first quarter of 2021, Robinhood reported $331 million in payment for order flow revenue. We estimate that the profits from this type of back-running (that is, inferring institutional order flows from retail order flows) are one order of magnitude larger, in billions of dollars per year. Institutional investors may have adapted to HFT back-runners, and it is time for them to pay attention to back-running via retail order flow as well.

[1] Ernst, T., J. Sokobin, and C. Spatt. 2021. The Value of Off-Exchange Data. Working Paper, University of Maryland.

Professor of Finance and Professor of Economics

Peter L. Mitchelson/SIT Investment Associates Foundation Chair in Investment Strategy

Bank of Canada Fellow

Rotman School of Management, University of Toronto